Compare providers

Download our outplacement comparison sheet

Request pricing

Compare our rates to other providers

Mergers and acquisitions (M&A) can be some of the most exciting and pivotal times at an organization. With so much at stake in M&A deals, it’s important that your organization be prepared to handle the process thoroughly and correctly. This includes drafting and delivering a well-written letter of intent M&A.

In this article, we’ll cover what a good M&A letter of intent example looks like, what it should include, why you need one, and how to customize and compose your own version for your organization’s M&A needs.

Letter of Intent M&A Sample

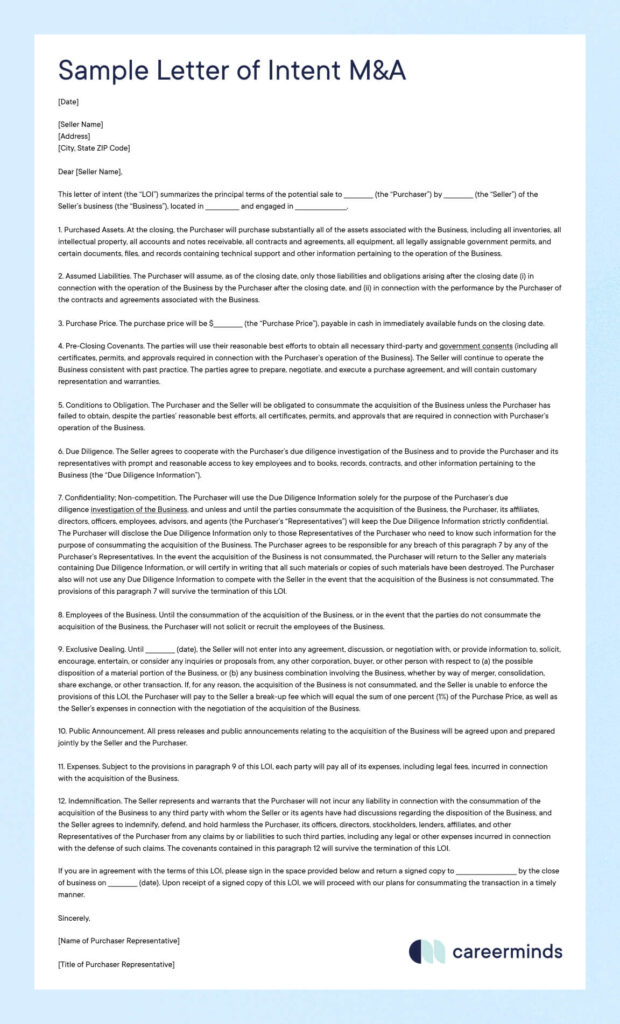

We’ll start with an M&A letter of intent example that you can copy and customize for your own letter of intent M&A needs. You’ll notice that there isn’t a lot of fluff or small talk in this template. Just as with other important M&A documentation, such as the client announcement letter, you want to get right to the point in your letter of intent to clearly and succinctly convey all of the proposed M&A deal details. So let’s illustrate how you might best put all of this into a letter of intent M&A sample.

Copyable example

[Date]

[Seller Name]

[Address]

[City, State ZIP Code]

Dear [Seller Name],

This letter of intent (the “LOI”) summarizes the principal terms of the potential sale to _____________ (the “Purchaser”) by _____________ (the “Seller”) of the Seller’s business (the “Business”), located in _______________ and engaged in _______________________.

1. Purchased Assets. At the closing, the Purchaser will purchase substantially all of the assets associated with the Business, including all inventories, all intellectual property, all accounts and notes receivable, all contracts and agreements, all equipment, all legally assignable government permits, and certain documents, files, and records containing technical support and other information pertaining to the operation of the Business.

2. Assumed Liabilities. The Purchaser will assume, as of the closing date, only those liabilities and obligations arising after the closing date (i) in connection with the operation of the Business by the Purchaser after the closing date, and (ii) in connection with the performance by the Purchaser of the contracts and agreements associated with the Business.

3. Purchase Price. The purchase price will be $_____________ (the “Purchase Price”), payable in cash in immediately available funds on the closing date.

4. Pre-Closing Covenants. The parties will use their reasonable best efforts to obtain all necessary third-party and government consents (including all certificates, permits, and approvals required in connection with the Purchaser’s operation of the Business). The Seller will continue to operate the Business consistent with past practice. The parties agree to prepare, negotiate, and execute a purchase agreement, and will contain customary representation and warranties.

5. Conditions to Obligation. The Purchaser and the Seller will be obligated to consummate the acquisition of the Business unless the Purchaser has failed to obtain, despite the parties’ reasonable best efforts, all certificates, permits, and approvals that are required in connection with Purchaser’s operation of the Business.

6. Due Diligence. The Seller agrees to cooperate with the Purchaser’s due diligence investigation of the Business and to provide the Purchaser and its representatives with prompt and reasonable access to key employees and to books, records, contracts, and other information pertaining to the Business (the “Due Diligence Information”).

7. Confidentiality; Non-competition. The Purchaser will use the Due Diligence Information solely for the purpose of the Purchaser’s due diligence investigation of the Business, and unless and until the parties consummate the acquisition of the Business, the Purchaser, its affiliates, directors, officers, employees, advisors, and agents (the Purchaser’s “Representatives”) will keep the Due Diligence Information strictly confidential. The Purchaser will disclose the Due Diligence Information only to those Representatives of the Purchaser who need to know such information for the purpose of consummating the acquisition of the Business. The Purchaser agrees to be responsible for any breach of this paragraph 7 by any of the Purchaser’s Representatives. In the event the acquisition of the Business is not consummated, the Purchaser will return to the Seller any materials containing Due Diligence Information, or will certify in writing that all such materials or copies of such materials have been destroyed. The Purchaser also will not use any Due Diligence Information to compete with the Seller in the event that the acquisition of the Business is not consummated. The provisions of this paragraph 7 will survive the termination of this LOI.

8. Employees of the Business. Until the consummation of the acquisition of the Business, or in the event that the parties do not consummate the acquisition of the Business, the Purchaser will not solicit or recruit the employees of the Business.

9. Exclusive Dealing. Until _____________ (date), the Seller will not enter into any agreement, discussion, or negotiation with, or provide information to, solicit, encourage, entertain, or consider any inquiries or proposals from, any other corporation, buyer, or other person with respect to (a) the possible disposition of a material portion of the Business, or (b) any business combination involving the Business, whether by way of merger, consolidation, share exchange, or other transaction. If, for any reason, the acquisition of the Business is not consummated, and the Seller is unable to enforce the provisions of this LOI, the Purchaser will pay to the Seller a break-up fee which will equal the sum of one percent (1%) of the Purchase Price, as well as the Seller’s expenses in connection with the negotiation of the acquisition of the Business.

10. Public Announcement. All press releases and public announcements relating to the acquisition of the Business will be agreed upon and prepared jointly by the Seller and the Purchaser.

11. Expenses. Subject to the provisions in paragraph 9 of this LOI, each party will pay all of its expenses, including legal fees, incurred in connection with the acquisition of the Business.

12. Indemnification. The Seller represents and warrants that the Purchaser will not incur any liability in connection with the consummation of the acquisition of the Business to any third party with whom the Seller or its agents have had discussions regarding the disposition of the Business, and the Seller agrees to indemnify, defend, and hold harmless the Purchaser, its officers, directors, stockholders, lenders, affiliates, and other Representatives of the Purchaser from any claims by or liabilities to such third parties, including any legal or other expenses incurred in connection with the defense of such claims. The covenants contained in this paragraph 12 will survive the termination of this LOI.

If you are in agreement with the terms of this LOI, please sign in the space provided below and return a signed copy to ___________________________ by the close of business on _____________ (date). Upon receipt of a signed copy of this LOI, we will proceed with our plans for consummating the transaction in a timely manner.

Sincerely,

[Name of Purchaser Representative]

[Title of Purchaser Representative]

Before we break down this M&A letter of intent example into the nitty gritty of what purpose it serves and what to include in your own letter of intent M&A, you can click below to download a free PDF version of this M&A letter of intent example and our complete guide to smoothly navigate the merger and acquisition process from start to finish.

What Is an LOI in Business Acquisition?

In a merger or acquisition, an M&A letter of intent is used to determine the terms and the timing of the deal, as well as make sure that the seller will stop talking with other buyers. If the next part of the process goes smoothly, wherein the seller goes through due diligence and the buyer acquires capital to make the purchase, then the transaction will be complete.

However, it’s also important to remember that a letter of intent is not a guarantee. Some parts of the letter—such as confidentiality clauses—may be more enforceable than others, but the overall document isn’t a final agreement for the M&A sale. If the deal falls through or goes to court, the letter of intent will not serve as any sort of enforceable contract.

Instead, the letter of intent M&A language is designed to be a non-binding proposal for the final deal agreement, outlining the proposed price and terms for the buyer to purchase the seller’s business. It signals the start of the M&A process, so the overall deal will not be finalized through this document.

Why Is It Important to Have a Letter of Intent M&A?

A letter of intent in M&A is essential as it lays out the foundation for the final deal that will be struck. Think about when you go to a car dealership, and you see the numbers listed on the cars. That number lays the foundation for where you will start the negotiation process. It is the starting point for where the final deal will end up.

An M&A letter of intent works in a similar fashion. Not only does it provide a starting place as far as pricing and timing, but it also allows both the buyer and seller to create stipulations that protect themselves throughout the remainder of the merger and acquisition process.

For buyers, the letter of intent M&A is important because it allows them to have an exclusivity period where the seller won’t talk to any other buyers on the market. This is the equivalent to taking your house off the market while someone does a final check of the property before signing on the dotted line.

For sellers, the letter of intent M&A is equally important. It can provide confidentiality protection for both parties when discussing sensitive information. If this particular deal was to fall through, you wouldn’t want the old buyers to give information to new buyers that could ruin your negotiation. It also protects against leaked information about the inner workings of your company that could hurt your public image and brand, and decrease your valuation in future attempts to sell.

What Should Be Included in a Letter of Intent M&A?

There are standard things that most companies always include in a letter of intent. However, you will want to check with your legal counsel to ensure that the specific items on your M&A letter of intent make sense for your situation. We aren’t attorneys, and there is a great deal of capital and jobs on the line with a merger or acquisition. So it is extremely important that you review any M&A documentation with a legal professional.

Here are the key sections that a letter of intent in M&A commonly includes:

- Purchased assets

- Assumed liabilities

- Purchase price

- Pre-closing covenants

- Conditions to obligations

- Due diligence

- Confidentiality and non-competition

- Employees

- Exclusivity

- Public announcement

- Expenses

- Indemnification

Let’s dig into each of these components a bit deeper to understand their purpose, as well as how they will apply specifically to your organization.

1. Purchased Assets

This section of the letter of intent in M&A refers to the purchaser’s intent to acquire all of the assets belonging to the seller’s company at the point of transaction. This means that the purchaser can’t only buy a part of the organization, such as only the intellectual property, but rather must purchase all of the organization’s assets as part of the deal. This includes equipment, intellectual property, records, office locations, etc.

This is typically standard, though there are of course situations where the purchaser and seller might agree to a purchase of only certain select assets. In that case, it’s especially important to have your legal counsel draft this section of the letter to thoroughly and correctly lay out those details.

2. Assumed Liabilities

This part of the letter determines how liabilities will be handled according to the M&A transaction. Generally, the purchaser agrees to assume all liabilities and obligations of the seller’s business after the purchasing date. This is to protect the purchaser from taking on any costly liabilities or obligations that occurred before the actual purchase of the organization which they may have been unaware of at the time.

Again, the above language is standard, but there may be situations in which the purchaser agrees to take on any and all liabilities or obligations that occur as part of the M&A agreement. If so, you will want your legal counsel to help you take this into consideration when drafting the M&A letter of intent.

3. Purchase Price

This part of the letter of intent M&A sample is fairly straightforward. It states the proposed purchase price for the seller’s business based on the valuation process and negotiations, and how and when that amount should be paid out by the purchaser. Some deals will stipulate a full cash amount payable at the time of transaction, while other deals might have a two-year payment plan, or not require the funds to be entirely in cash.

4. Pre-Closing Covenants

This segment of the letter contains promises that the purchaser and seller make to each other before the M&A transaction is complete. This can include a promise on both sides of the deal to obtain all necessary licenses and government certificates, as well as a promise by the seller to continue to run the business in accordance with how it has been run in the past.

5. Conditions to Obligation

This section of the letter is also fairly short and simple, describing the obligations of the purchaser and seller to finalize the M&A deal, except in the event that certain factors have not been met, such as the purchaser failing to obtain necessary government approval, licenses, or certificates.

6. Due Diligence

The due diligence process is very important to the success of a merger or acquisition. During this process, the purchaser audits every aspect of the seller’s business to ensure that the deal will be successful in the long run. In this part of the M&A letter of intent, the seller agrees to cooperate with the purchaser’s auditors and due diligence process.

7. Confidentiality and Non-Competition

This is an especially important part of a letter of intent in M&A. Its purpose is to ensure the confidentiality of any and all information that the purchaser finds during their due diligence process, and keep it so either until the deal is finalized or in perpetuity if the deal doesn’t go through. This confidentiality can be further protected with an additional non-disclosure agreement, but it’s good to lay the groundwork for this in the letter of intent. This section can also require that the purchaser does not use such due diligence information to compete with the seller in the event the deal doesn’t go through.

8. Employees

This segment of the M&A letter of intent is also pretty straightforward and similar to the confidentiality/non-compete section. It essentially states that the purchasing organization will not try to poach any employees away from the selling organization under any circumstance, either leading up to the transaction or afterwards if the deal falls through. Obviously, this won’t matter if the M&A deal is finalized and the post-merger integration process begins.

9. Exclusivity

This section of the letter guarantees that the seller will not entertain any other purchasers while the due diligence and final negotiations of the M&A deal are taking place. In exchange for this exclusivity, the purchaser will generally need to agree to some sort of financial incentive that they would owe to the seller if they ultimately back out of the deal.

10. Public Announcement

Since mergers and acquisitions are generally announced to the press at some point during the finalization of the deal, this portion of the letter proposes how the deal will be announced, and who will be responsible for the creation of the announcement. Generally, both parties will collaborate on this announcement together.

11. Expenses

This section of the M&A letter of intent states that both parties will be responsible for all of their own expenses and fees associated with the merger or acquisition, except as otherwise stated in other provisions of the letter.

12. Indemnification

This section states that the seller of the business understands that the purchaser will not have any liability in paying any third parties that helped assist the seller throughout the M&A deal, such as legal expenses or auditors.

M&A Letter of Intent: Final Takeaways

If you cover all of these letter of intent M&A sample sections, you’ll be well on your way to having your own great letter of intent for your merger or acquisition. Now, it’s important to mention that M&As are very tricky events. You will need to work closely with your M&A deal team, as well as with the other company’s team and management, and—perhaps most importantly—your legal counsel as you prepare all of the necessary documentation and details of the deal.

At Careerminds, we believe that you can never be too prepared for your next major business event, especially any that might result in workforce reductions. Our arsenal of resources, templates, guides, and industry-leading outplacement services can help you navigate the delicate integration or reduction process. Click below to speak with one of our experts and see if we are the right partner for your organization.

bring the CHALLENGE.

wE have the SOLUTION.

Protect your brand and support your people through change. From career transition to leadership development, we bring clarity and care to the moments that matter most.